Jason paid on time, yet he was still charged interest.

Jason believed he was managing his credit card responsibly by paying on time and never missing a due date, assuming this would prevent interest charges. However, he was surprised to find an interest charge on his statement. After contacting his bank, he learned he had lost his grace period, which allowed interest to accrue on his purchases despite timely payments. This misunderstanding ultimately cost him hundreds of dollars.

Many credit card users make the same mistake, unaware that the key to saving money is understanding the credit card grace period. This brief window determines whether purchases remain interest-free or begin to accrue additional costs.

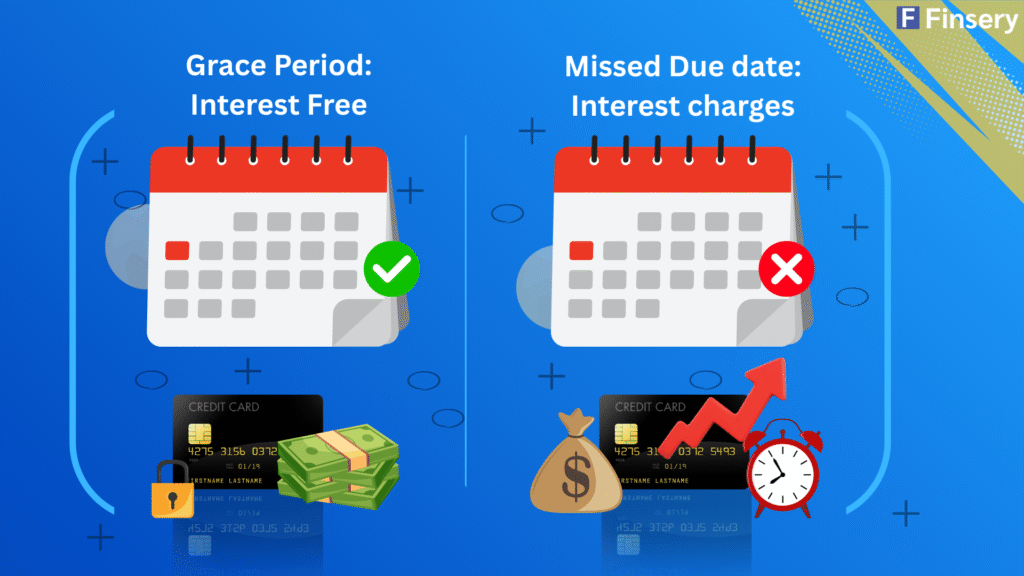

Jason’s experience highlights the importance of timing in avoiding late fees and maintaining a budget. The period between a statement and its due date, known as the grace period, is key to managing credit cards effectively. Understanding how this payment window works can help you avoid interest charges.

What Is a Grace Period on a Credit Card?

The grace period is the time between your statement date and your payment due date during which no interest accrues. You can pay your statement balance during this period without incurring interest. This feature offers valuable flexibility for repaying your balance.

In the U.S., grace periods typically range from 21 to 25 days. These periods apply only to standard purchases, not to cash advances, balance transfers, or any transaction where interest accrues immediately.

How the Grace Period Works in a Billing Cycle

Your credit card is billed monthly, not only on the payment due date. Each billing cycle includes an interest-free window that determines whether your purchases remain interest-free or begin accruing interest. Understanding the relationship between these dates is crucial for avoiding unnecessary interest charges

On the purchase date, you can use your credit card. Each purchase counts towards your current billing cycle. Purchases made early in the cycle receive more interest-free days than those made closer to the end.

The statement closing date is a significant milestone for your account. On this date, your card issuer finalizes the billing cycle and aggregates all transactions. This total becomes your statement balance, and the grace period subsequently commences.

This starts immediately after the statement closes. This interest-free window lasts from your statement date to your due date. Paying the full statement balance during this time avoids interest charges on purchases.

This period typically lasts at least 21 days on most cards, according to guidance from the Consumer Financial Protection Bureau.

On the payment due date, you use your credit card. Each purchase enters your current billing cycle. This is the final day to pay your statement balance to keep purchases interest-free. Paying only the minimum or paying late may result in losing your grace period, which affects how interest is applied in the future

If the statement balance is not paid in full by the due date:

-

Interest adds up every day.

- It is calculated using your credit card’s APR and average daily balance.

- New purchases may no longer get a interest-free window.

Many users are unaware that losing the grace period can cause interest to add up from the purchase date, not just after the due date.

Understanding the credit card billing cycle helps you avoid interest, plan purchases, and use your credit card as a short-term, interest-free payment tool rather than accumulating revolving debt.

When the Grace Period Does Not Apply

The credit card grace period allows you to avoid interest on eligible purchases; however, not all transactions qualify. Most cards apply the grace period only to standard purchases, while other transactions may accrue interest immediately.

| Transaction Type | Grace Period? | Interest Behavior |

|---|---|---|

| Purchases | Yes | Interest avoided |

| Cash Advances | No | Interest starts immediately |

| Balance Transfers | Usually no | Depends on promo terms |

| Some Promotions | Not true grace | Interest may be deferred |

Understanding these exceptions is crucial to avoiding credit card interest charges.

- Purchases: Foreign transactions are treated as standard purchases and may qualify for the credit card’s interest-free benefit if you pay the full statement balance on time. Foreign transaction fees and currency conversion charges may still apply and are separate from interest charges. If you have lost your grace period by carrying a balance, interest on these transactions will accrue immediately.

- Cash Advances: Withdrawing cash from your credit card at an ATM, at a bank, or by using convenience checks is considered a cash advance. These transactions do not have a grace period, and interest begins accruing immediately, making them more expensive than regular purchases.

- Balance Transfers: Moving debt from one credit card to another is a balance transfer. Unless a 0% promotional offer applies, interest typically starts accruing immediately. Even with a promotion, transferred balances follow different interest rules and do not receive a standard grace period.

- Some Promotional Offers: Certain “no interest” financing offers do not provide a regular grace period. Instead, interest is deferred until a set deadline. If the balance is not paid in full by that date, all accumulated interest may be charged at once, making these offers riskier than standard interest-free periods.

How the Grace Period Saves You Money

One of the best perks of a credit card grace period is that it helps you avoid interest charges! When you pay your full statement balance by the due date, you can enjoy interest-free spending. And since credit card APRs can soar above 20%, even tiny balances can become pricey. By using this feature, your credit card becomes a powerful short-term payment tool that helps you manage your finances with confidence and effectiveness.

Besides direct interest savings, the grace period also supports:

- Better cash flow management. You can cover expenses now and pay later at no additional cost, helping stabilize your monthly budget.

- Stronger credit health. Consistently paying the full statement balance demonstrates responsible use, keeps balances low, and can improve your credit profile over time.

Finsery pro tip

The grace period usually applies only when the previous statement balance is paid in full. Miss that once, and interest can start immediately on new charges.

Grace Period vs Due Date: Understanding the Key Difference

The grace period and the payment due date are often mistaken for the same; however, they serve distinct functions within the credit card billing cycle. This misunderstanding may lead to unexpected interest charges, even when payments are made on time. Clarifying the distinction between the grace period and the due date can help cardholders avoid unnecessary interest fees and late charges.

The grace period relates to interest, while the due date is when your payment is due. They are linked, but not the same thing.

| Feature | Grace Period | Due Date |

|---|---|---|

| Main Purpose | Interest-free window on purchases | Final day to make at least the minimum payment |

| What It Protects You From | Credit card interest charges | Late fees and penalty APRs |

| When It Starts | Right after the statement closing date | Set calendar date each billing cycle |

| When It Ends | On the payment due date | Same date each month |

| What Happens If Missed | Interest begins accruing on purchases | Late fee charged and possible credit score impact |

| Eligibility | Only if previous balance was paid in full | Applies to all cardholders every month |

What Happens if You Miss the Grace Period

It’s important to be mindful of your credit card’s grace period! If missed, you could see interest accrue more quickly than expected. By not paying the full statement balance by the due date, you forfeit the interest-free advantage, turning your card from a short-term, cost-free option into revolving debt. Staying on top of your payments can really help you manage your finances positively!.

The following outlines the subsequent steps in the credit card interest timeline:

- Daily Interest Begins: Interest is calculated daily based on your average daily balance. Each day you carry a balance, additional interest accrues.

- Your APR Is Applied: Your card’s Annual Percentage Rate (APR) is converted to a daily rate and applied to your balance. Since many credit cards have APRs above 20%, even small balances can increase rapidly.

- Your Statement Balance Grows: As interest accrues on your existing balance, the total amount owed increases. If you continue to carry a balance, future interest is calculated on this higher amount.

- The Debt Snowball Effect: At this stage, compounding works against you. Interest accrues on prior interest, making it more difficult to pay off your balance over time. A manageable amount can become long-term debt if not addressed promptly.

If you miss the grace period, your account enters an interest-accruing cycle. Paying the full statement balance on time is essential to avoid ongoing credit card interest.

Practical tips to maximize your credit card grace period

Understanding a credit card’s grace period is just the first step. Using it effectively can help you avoid interest charges. Experienced cardholders view the grace period as a timing tool, not just a window for making payments. Here are some strategies to maximize its benefits.

1. Plan Large Purchases at the Start of Your Billing Cycle

The timing of your purchase significantly influences your interest-free period. When you make a purchase just after your statement closing date, you can take advantage of nearly a full billing cycle plus the grace period, potentially extending your interest-free period to almost 50 days before interest begins to accrue.

This strategy not only maximizes your interest-free period but also provides ample time to pay without incurring additional costs. It’s a powerful approach to enhancing your cash flow and effectively avoiding interest charges.

2. Automate Full Statement Balance Payments

Setting up automatic payments for your full statement balance, rather than just the minimum due, helps you maintain your interest-free period each month. Paying in full by the due date prevents new purchases from accruing interest, while missing a full payment can result in immediate interest charges. Automation also reduces the risk of late fees, preserves your eligibility for interest-free purchases, and encourages responsible credit use. In summary, automating payments makes interest avoidance a reliable process instead of a monthly task to remember.

3. Avoid Cash Advances Whenever Possible

Cash advances do not qualify for a grace period, so interest accrues immediately upon withdrawal, often at a higher Annual Percentage Rate (APR) than for regular purchases.

Using a credit card for cash can rapidly eliminate the benefits of your grace period. If you need funds, explore better options, such as debit withdrawals or more cost-effective borrowing alternatives.

Jason’s mistake is common. His fix is simple.

Jason’s problem wasn’t overspending; it was all about timing. When he learned how the credit card grace period worked, he began paying his full statement balance and paying attention to the statement date as well as the due date. His interest charges disappeared, even though he spent the same amount.That’s the benefit of the grace period. When you know how it works, you can keep your purchases interest-free instead of letting them turn into debt.

At Finsery, we want to make these hidden rules easier to understand so credit card users can pick the right cards, use them wisely, and avoid unnecessary risks. Even small gaps in knowledge can become expensive over time, but having the right information when you need it can help protect your finances for years

Frequently Asked Questions

Back to topNo. If you carry a balance from the previous billing cycle, most card issuers remove the grace period on new purchases, and interest may start accruing immediately.

Even if you paid by the due date, interest may still be charged if you did not pay the full statement balance or if you lost your grace period in a previous cycle. This can happen even when there is no late fee.

No. Purchases made earlier in the billing cycle get more interest-free days than those made right before the statement closes.

Most cards provide at least 21 days between the statement date and the due date, though the total interest-free time can be longer depending on when a purchase is made.

No. Paying only the minimum keeps the account from being late but usually causes you to lose your interest-free grace period.

They may start accruing interest immediately until you fully pay off the balance and restore your grace period.