Best Credit Cards for Beginners to Build Credit

If you’re starting your credit journey, the right first credit card can help you build a strong credit score, qualify for better financial products, and avoid costly mistakes. The best beginner credit cards in 2026 prioritize approval accessibility, low fees, and credit-building features over rewards. After reviewing beginner-friendly cards based on approval difficulty, fees, credit reporting policies, and upgrade options, these are the best credit cards for building credit.

1. Capital One Platinum Secured Credit Card

The Capital One Platinum Secured Credit Card is a highly accessible option for those new to building credit. Its refundable security deposit makes approval easier than with traditional unsecured cards, making it an effective choice for individuals with no credit history.

Credit Building Program

This card is designed to help users build or rebuild credit through responsible use and on-time payments. Account activity is reported to all three major credit bureaus.

| Benefit | Value | Details |

|---|---|---|

| Security Deposit | $49–$200 | Refundable deposit starting at $49 may qualify you for a $200 credit line. |

| Credit Line Review | 6 months | Automatic consideration for credit line increase after responsible use. |

| Fraud Protection | $0 | Zero liability protection against unauthorized charges. |

| Credit Monitoring | Free CreditWise | Free credit monitoring tools available. |

Pros

- Credit line review opportunity

- Low minimum deposit

- Helps build credit

- Fraud protection

- No annual fee

Cons

- Security deposit required

- No rewards program

- Low starting limit

- High APR

The yearly fee charged to keep the card active.

A recurring monthly charge for this card.

Fee charged when transferring balances from another card.

Additional fee for purchases processed in foreign currencies.

Fee charged when withdrawing cash from your credit line.

Penalty fee if your payment is made after the due date.

Standard APR applied to regular purchases.

APR applied to balance transfers.

APR charged on cash advances, usually higher than regular APR.

Higher APR that can apply after late or missed payments.

Promotional APR available for an introductory period.

How long the introductory APR remains in effect.

Requirements

Additional Information

The Capital One Platinum Secured Credit Card is designed for individuals who are building or rebuilding their credit. With a low minimum deposit and no annual fee, it provides an accessible path to establishing a positive credit history.

Why we picked it : Secured credit cards are a good option for beginners, as the deposit serves as collateral, reducing the issuer’s risk. Responsible use helps you build payment history, and you may qualify for a refund and account upgrade over time.

2. Discover it® Student Cash Back

The Discover it Student Cash Back card is a leading choice for students, offering both credit-building features and cashback rewards. Unlike many entry-level cards, it enables users to earn rewards while building their credit history.

Discover Cashback Bonus®

Earn cashback rewards while building credit. Discover matches all cashback earned during the first year and rewards never expire while the account is active.

| Category | Reward Rate | CAP |

|---|---|---|

| Gas Stations |

2%

Up to $1,000

|

Quarterly cap applies |

| Restaurants |

2%

Up to $1,000

|

Quarterly cap applies |

| All Other Purchases |

1%

Default rewards

|

Unlimited |

Pros

- Cashback rewards uncommon for secured cards

- First-year rewards match

- Refundable deposit

- Helps build credit

- No annual fee

Cons

- Limited acceptance vs Visa

- Requires responsible use

- Security deposit required

- High APR

The yearly fee charged to keep the card active.

A recurring monthly charge for this card.

Fee charged when transferring balances from another card.

Additional fee for purchases processed in foreign currencies.

Fee charged when withdrawing cash from your credit line.

Penalty fee if your payment is made after the due date.

Standard APR applied to regular purchases.

APR applied to balance transfers.

APR charged on cash advances, usually higher than regular APR.

Higher APR that can apply after late or missed payments.

Promotional APR available for an introductory period.

How long the introductory APR remains in effect.

Requirements

Additional Information

The Discover it® Secured Credit Card is one of the few secured cards offering rewards and no annual fee. With cashback earnings and credit bureau reporting, it is widely considered one of the best cards for beginners building credit.

Why we picked it: We chose this card because it allows students to build credit while earning cashback rewards, including Discover’s first-year Cashback Match, which can significantly increase the value of rewards for beginners.

3. Chase Freedom Rise®

The Chase Freedom Rise is intended for individuals new to credit who seek an unsecured card without a security deposit. It also offers cashback rewards, adding value for those starting to build credit.

Chase Ultimate Rewards® Cashback

Earn 1.5% cash back on all purchases while building credit. Rewards do not expire as long as the account remains open and there is no minimum redemption requirement.

| Category | Reward Rate | CAP |

|---|---|---|

| Lyft Rides |

2%

Limited time offer

|

Offer terms apply |

| All Purchases |

1.5%

Unlimited rewards

|

No limit |

Pros

- Credit building features

- Beginner friendly card

- Upgrade opportunity

- Cashback rewards

- No annual fee

Cons

- Requires Chase relationship improves approval

- Limited benefits vs premium cards

- Foreign transaction fee

- No bonus categories

The yearly fee charged to keep the card active.

A recurring monthly charge for this card.

Fee charged when transferring balances from another card.

Additional fee for purchases processed in foreign currencies.

Fee charged when withdrawing cash from your credit line.

Penalty fee if your payment is made after the due date.

Standard APR applied to regular purchases.

APR applied to balance transfers.

APR charged on cash advances, usually higher than regular APR.

Higher APR that can apply after late or missed payments.

Promotional APR available for an introductory period.

How long the introductory APR remains in effect.

Requirements

Additional Information

The Chase Freedom Rise® card is designed for people new to credit who want to earn simple cashback while building a credit history. With no annual fee and credit-building tools, it serves as a strong starter card.

Why we picked it: We selected this card because it is an unsecured starter card with no annual fee, making it a strong option for beginners who want to build credit without paying a security deposit, especially those with an existing Chase banking relationship.

4. Capital One Quicksilver Student Cash Rewards

The Capital One Quicksilver Student card is a strong option for new-to-credit-card users who prefer a straightforward rewards structure. It provides a flat cashback rate on all purchases, eliminating the need to track rotating categories.

Capital One Cashback Rewards

Earn unlimited 1.5% cash back on every purchase with no rotating categories or spending limits. Rewards do not expire as long as the account remains open.

| Category | Reward Rate | CAP |

|---|---|---|

| Capital One Travel |

5%

Travel bookings portal

|

No limit |

| All Purchases |

1.5%

Unlimited rewards

|

No limit |

Pros

- No foreign transaction fees

- Simple cashback rewards

- Signup bonus available

- Helps build credit

- No annual fee

Cons

- Limited premium benefits

- No bonus categories

- No intro APR

- High APR

The yearly fee charged to keep the card active.

A recurring monthly charge for this card.

Fee charged when transferring balances from another card.

Additional fee for purchases processed in foreign currencies.

Fee charged when withdrawing cash from your credit line.

Penalty fee if your payment is made after the due date.

Standard APR applied to regular purchases.

APR applied to balance transfers.

APR charged on cash advances, usually higher than regular APR.

Higher APR that can apply after late or missed payments.

Promotional APR available for an introductory period.

How long the introductory APR remains in effect.

Requirements

Additional Information

The Capital One Quicksilver Student card is a good choice for students looking to build credit while earning simple cashback rewards. With no annual fee and easy rewards structure, it is a practical starter card for college students.

Why we picked it: We chose this card for its simple flat-rate cashback rewards, making it ideal for beginners who want an easy-to-understand rewards structure while building their credit history.

5. OpenSky® Secured Visa® Credit Card

The OpenSky Secured Visa Credit Card is frequently recommended for individuals who may face challenges obtaining approval elsewhere. Because it does not require a traditional credit check, it serves as a practical option for those without an established credit profile.

We may receive compensation when you apply through our links. Offers and terms change; confirm details on the issuer's site before applying.

Credit Builder Program

The OpenSky® Secured Visa® Credit Card helps individuals build or rebuild credit through responsible use. The card reports account activity to all three major credit bureaus and does not require a credit check to apply.

| Benefit | Value | Details |

|---|---|---|

| Security Deposit | $200 minimum | Refundable deposit determines your credit limit. |

| Upgrade Opportunity | - | May qualify for unsecured card after responsible use. |

Pros

- No credit check required

- Flexible deposit amount

- Reports to all bureaus

- Easy approval odds

- Helps build credit

Cons

- Security deposit required

- No rewards program

- Annual fee required

- High APR

The yearly fee charged to keep the card active.

A recurring monthly charge for this card.

Fee charged when transferring balances from another card.

Additional fee for purchases processed in foreign currencies.

Fee charged when withdrawing cash from your credit line.

Penalty fee if your payment is made after the due date.

Standard APR applied to regular purchases.

APR applied to balance transfers.

APR charged on cash advances, usually higher than regular APR.

Higher APR that can apply after late or missed payments.

Promotional APR available for an introductory period.

How long the introductory APR remains in effect.

Requirements

Additional Information

The OpenSky® Secured Visa® Credit Card is designed for people with poor or limited credit who may not qualify for traditional cards. With no credit check and a refundable deposit, it provides an accessible path to building credit history.

Why we picked it: We chose this card because it offers easy approval with no credit check, making it a practical option for individuals with no credit history or those looking to build credit from scratch.

How We Chose the Best Beginner Credit Cards

Our editorial team reviewed dozens of starter credit cards from major issuers to identify the best options for beginners. We prioritized cards that are accessible to new credit users and offer strong credit-building potential and long-term value.

We focused on accessibility for beginners rather than on premium rewards, as approval and credit-building are more important when starting out. This method aligns with major financial publishers, who evaluate starter cards based on eligibility, fees, and credit-building features.

Primary Factors

We prioritized these factors because they directly affect a beginner’s ability to qualify for a card and build credit.

- Approval difficulty – We focused on cards designed for applicants with no credit, limited credit, fair credit, or student profiles.

- Annual fees – We preferred cards with no or low annual fees to minimize costs for beginners.

- Credit bureau reporting – Only cards that report to all three major credit bureaus (Experian, Equifax, and TransUnion) were considered.

- Upgrade opportunities – We rated cards higher if they offer graduation to unsecured cards, credit limit increases, or product upgrades.

- Security deposit requirements – For secured cards, we evaluated minimum deposits, flexibility, and refund policies.

- Issuer reliability – We preferred established issuers with strong customer support and security standards.

- Interest rates (APR) – Although beginners should avoid carrying balances, we ranked cards with excessively high APRs lower.

Secondary Factors

These factors were used to differentiate cards once primary requirements were satisfied:

- Rewards structure – Cashback or straightforward rewards programs were viewed as additional benefits rather than primary considerations.

- Mobile app features – Account management, payment alerts, and spending trackers.

- Credit monitoring tools – Free credit score access and educational resources were considered beneficial.

- Customer experience – Issuer reputation, service quality, and overall user experience were evaluated.

- Fraud protection features – Zero liability coverage and transaction alerts.

- Financial education tools – Cards providing educational resources for beginners received additional consideration.

- Account management flexibility – Autopay options, due date flexibility, and digital statements.

- Foreign transaction fees – Considered for beginners who may travel or make international purchases.

How to Choose the Right First Credit Card

Choosing your first credit card is less about maximizing rewards and more about finding a card you can qualify for and use to build a strong credit foundation. The right beginner credit card should match your financial situation, approval chances, and long-term credit goals. If you’re new to credit, focus on these key decision factors before applying. You can also read our detailed guide on how to choose a credit card to understand key features, fees, and eligibility factors before making a decision.

How Beginners Can Build Credit Faster

When used responsibly, your first credit card can help you establish a credit profile within months and improve your credit score within the first year. Since credit scores depend on payment history, credit usage, and account age, beginners can make steady progress by adopting disciplined habits.

Follow these proven strategies to build credit faster and avoid common beginner mistakes:

Your payment history is the most important factor in your credit score. Even one late payment can negatively affect your score and remain on your credit report for years.

Consider the following best practices:

- Pay at least the minimum amount due each month.

- Submit payments before the due date rather than waiting until the last day.

- Set reminders to ensure timely payments.

- Enable automatic payments when available.

- Avoid missing payments at any time.

Setting up autopay for at least the minimum amount helps prevent accidental late payments while you pay the full balance manually.

Credit utilization, or the percentage of your credit limit used, is a key factor in your credit score. Experts recommend keeping usage below 30% of your limit.

Example:

Credit limit → $500

Ideal usage → Under $150

Excellent usage → Under $100

Lower utilization demonstrates responsible credit management and may help improve your score more quickly.

Best practices:

- Consider making several small payments throughout the month.

- Avoid using your full credit limit.

- Request a credit limit increase after establishing a positive payment history.

- Spend only what you can afford to pay off immediately.

Even if you pay your balance in full, reaching your credit limit during the month may still affect your score if a high balance is reported.

Many payment errors occur when individuals miss due dates. Setting up autopay is an effective way to safeguard your credit score.

Autopay offers several benefits:

- Avoid late fees

- Protect your payment history.

- Maintain a positive record.

- Reduce financial stress.

The recommended approach is to set autopay for the minimum payment as a backup, and manually pay the full balance before the due date.This strategy provides both flexibility and protection.

You do not need to make large purchases to build credit. Small, consistent transactions are often more effective.

Good beginner usage examples:

- Streaming subscriptions

- Mobile bills

- Fuel purchases

- Groceries

- Online subscriptions

The objective is to demonstrate consistent usage and responsible repayment.

Select one or two recurring expenses and use your credit card exclusively for these payments.

The length of your credit history impacts your credit score. Closing your first card early may decrease your average account age and lower your score.

Best practices:

- Keep your first credit card active.

- Use it periodically to prevent closure due to inactivity.

- Avoid closing your oldest account.

- Consider upgrading your card rather than closing it, if possible.

Even if you obtain better cards later, keeping your first card open supports a longer credit history.

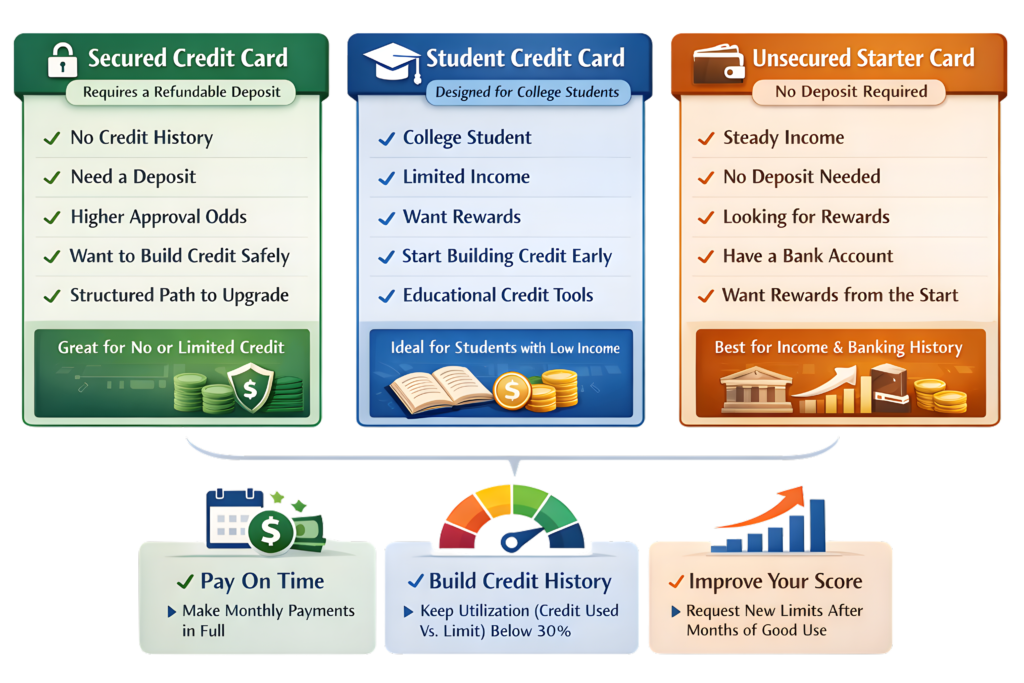

Who Should Apply for a Beginner Credit Card?

Beginner credit cards are intended for individuals new to credit or with limited credit history. These cards generally offer easier approval and help users build a solid financial foundation.

- First-time credit users: If you have never used credit before, a beginner credit card can help you establish your credit profile. Responsible use, including timely payments and low balances, can generate your first credit score within a few months. This is often the first step toward qualifying for more favorable financial products.

- Students: Students often have limited income and no credit history, making beginner or student credit cards a practical starting point. These cards typically feature easier approval and may offer educational resources. Building credit early helps students establish a strong credit history before entering the workforce.

- Young professionals: If you have recently started your first job, a beginner credit card can help you build financial credibility. With a steady income, you may also qualify for entry-level unsecured cards. Establishing credit early supports future loan, housing, and premium credit card approvals.

- Immigrants building U.S. credit: New immigrants often need to build credit from the beginning, as foreign credit history typically does not transfer to the U.S. system. Beginner credit cards, particularly secured cards, can help establish a new credit profile. This is important for renting housing, financing purchases, or qualifying for better financial products.

- Anyone with a thin credit history: Even with existing credit accounts, you may have a “thin credit file” if your history is limited. Beginner cards can strengthen your profile by adding positive payment history. Over time, this can improve your credit score and expand your financial opportunities.

Frequently Asked Questions

Back to topMost beginner credit cards are designed for people with no credit history or limited credit profiles. Secured and student cards usually do not require an existing credit score for approval. Some unsecured starter cards may require fair credit or proof of income. Choosing a card designed for beginners improves approval chances.

Most beginners can generate a credit score within about 3 to 6 months of responsible usage. Noticeable improvements usually happen within 6 to 12 months if payments are made on time and balances remain low. Building excellent credit typically takes longer and depends on consistent habits. Regular usage and on-time payments are the biggest factors.

A secured credit card is often recommended if you have no credit history because approval is usually easier. These cards require a refundable deposit that becomes your credit limit. They help build payment history just like regular credit cards. Many secured cards also allow upgrades to unsecured cards later.

Most financial experts recommend starting with one credit card. Managing one account responsibly helps establish payment history without increasing financial risk. After building history for about 6–12 months, you may consider adding another card if needed. Applying for too many cards early can hurt approval chances.

Yes, some beginner cards offer cashback or basic rewards, especially student and entry-level unsecured cards. However, approval should be the main priority rather than rewards. Beginners should focus first on building credit before optimizing rewards. Better reward cards usually become available after credit improves.

The best approach is to use your card for small regular purchases and pay the full balance every month. Keeping your credit utilization below 30% and avoiding late payments can help improve your credit score faster. Monitoring your statements and setting autopay can also prevent mistakes. Responsible usage is the key to long-term credit growth.